Governor Hutchinson’s proposed changes to the state's Medicaid expansion received approval from both houses of the Arkansas Legislature on Tuesday. The governor wants to add work requirements to the program and to cut eligibility, removing around 60,000 Arkansans from Medicaid coverage, with the idea that they would move to the subsidized Affordable Care Act marketplaces or employer-sponsored plans. Once Hutchinson signs the legislation, the new policy will still require approval from the federal government.

Speaking before a joint session of the legislature, which reconvened on Monday for a special session, Hutchinson defended the eligibility cut, arguing that these 60,000 Arkansans "will not lose access to coverage" and would get "the same level of financial support that they have now." The truth is a little more complicated. The policy he is proposing would likely mean significant increases in costs for a population already struggling to make ends meet. Hutchinson's plan would also almost certainly lead to many of them losing insurance altogether. Let's take a look at some of the issues raised by booting more than 60,000 people off of the Medicaid rolls.

The governor's plan

Hutchinson wants to move people who make between 100-138 percent of the federal poverty level off of Medicaid and onto other coverage.

First, a quick refresher on the background: As part of the Affordable Care Act, Arkansas expanded Medicaid via a unique policy known as the private option, which uses Medicaid funds to purchase private health insurance plans for low-income Arkansans. The concept was later re-branded as "Arkansas Works" by the governor. The expansion covers adults who make less than 138 percent of the federal poverty level — that's $16,400 for an individual or $33,600 for a family of four.

The governor's proposed changes to eligibility removes anyone who makes more than the federal poverty line (that's $11,880 for an individual or $24,300 for a family of four) from the Arkansas Works program. Only people who make less than the poverty line would qualify going forward. That includes not just the beneficiaries who are covered by private option plans but also those who were deemed medically frail under Arkansas Works (the 10 percent of beneficiaries with the greatest medical needs, who are currently routed to the traditional Medicaid program rather than private option plans).

The population Hutchinson aims to cut — again, that's folks making between 100 and 138 percent of FPL — is comprised of tens of thousands of the state's working poor, who have gained affordable health coverage thanks to the Medicaid expansion. The governor wants to push them out of Medicaid and let them get coverage on the Obamacare marketplace (often called the exchange) or on employer-sponsored plans. Hutchinson says this will save the state $66 million over four years. While the federal government would have to pay more to cover those who go to the exchange, Hutchinson argues that because others will be moving to employer-sponsored insurance, the feds wouldn't incur any additional costs on net.

People will have to pay more in premiums on the exchange than they do today under "Arkansas Works."

Currently, under Arkansas Works, beneficiaries who make between 100-138 percent FPL are charged premiums at a flat rate of $13 per month.

The governor's core point is that if people move to the Obamacare exchange, they will get significant federal subsidies to help keep insurance affordable. The subsidies are designed so that premiums for what's known as the "benchmark plan" (the second cheapest Silver-level plan, which is equivalent to the plans that people on the private option currently have) will be 2 percent of monthly household income. Assuming that people who get moved to the exchange purchase plans similar to the private option plans, we already know approximately what premiums these folks will have to pay — 2 percent of their household income. A key point: Under current law, the premiums charged to this population would stay at that level even if the actual unsubsidized premium that insurance companies charge for the plan goes up or down.

The challenge for beneficiaries: That would be significantly more than $13 per month. An individual right at the poverty line might have to pay up to $20 a month in premiums. An individual who makes 138 percent FPL would have to pay up to $27 per month. Meanwhile, larger family sizes will have larger incomes in order to fall in the 100-138 FPL range. The exchange's premium credits are based on total income, meaning that people with larger households may have to pay more (kids in this income group would be covered by ARKids, but parents may be currently reliant on Arkansas Works). So a single mother of three, for example, who is right at the poverty line, would be on the hook for $40 per month premiums on the exchange; if she was at 138 percent FPL, she would be on the hook for $56 per month premiums.

A spokesperson for the Department of Human Services said that next year, Arkansas Works would have bumped premiums up to 2 percent of household income (the state's waiver to implement Arkansas Works does allow this). That's the basis for the governor's argument that premiums are staying the same if people move from Arkansas Works to the exchange going forward. But this year, in fact, premiums are a flat $13. Next year, if this population moves to the exchange via the governor's plan, all beneficiaries would see premiums increase and many would see that amount double, triple or more.

People will lose coverage if they can't pay.

Even assuming that Arkansas Works was going to move toward premiums that charged 2 percent of household income, there remains a mammoth difference between Arkansas Works premiums and those on the exchange. If people are unable to pay their premiums under Arkansas Works, they don't lose their coverage; they incur a debt to the state, which likely isn't very collectible unless there's a state tax refund from which to withhold. On the other hand, if people are unable to pay their premiums on the exchange, they'll be booted off of coverage and become uninsured for the remainder of the year. These premiums are relatively small, but this is a population with almost no disposable income. $40 a month may not sound like a lot, but for a family of four at the poverty line, that could be the difference in getting enough groceries to go around. Currently, only 25 percent of these beneficiaries are paying the $13 premiums each month. If these folks struggle to keep up with premiums on the exchange, they'll end up without coverage.

Many people will likely have to pay more in cost-sharing on the exchange, too.

Currently, Arkansas Works imposes nominal cost-sharing allowable under Medicaid rules to the 100-138 population. This cost-sharing is arranged so that the actuarial value of the plans covers 94 percent of medical costs. In other words, if you take the average medical costs for the standard population covered by the plan, the plan will pay for 94 percent of medical expenses, leaving enrollees paying the other 6 percent through the likes of co-pays.

If these people move to the exchange and purchase a Silver-level plan on the exchange, the federal government will provide cost-sharing-reduction subsidies to lower out-of-pocket costs. Normally, a Silver plan would have a 70 percent actuarial value, but for people at this income level, those cost-sharing reductions turn it into a 94 percent actuarial value, dramatically limiting how much people have to pay in deductibles, co-pays, and so on. This is why the governor claims that cost sharing is equivalent: In both cases, the plans have a 94 percent actuarial value.

However, there are a couple of differences. One is that the form of the cost-sharing is likely to be dramatically different. Under Medicaid rules, the Arkansas Works plans only have very small co-pays. On the exchange, insurance companies can use much more complex schemes, including deductibles. More importantly, the amount that sick people will be charged out of pocket will tend to be higher on the exchange. That's because Medicaid rules impose a strict limit on the total amount that beneficiaries can be charged between premiums and cost-sharing (it cannot exceed 5 percent of monthly or quarterly income). There is no such rule on the exchange, and while there are out-of-pocket limits, the total amount that beneficiaries have to pay could exceed 5 percent of income.

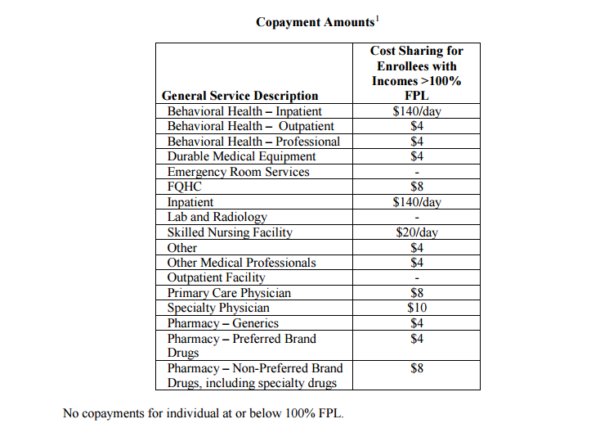

To compare, here is all of the cost-sharing currently imposed in Arkansas Works:

Meanwhile, on the exchange, Silver plans with cost-sharing-reduction subsidies for this population would impose deductibles and out-of-pocket maximum amounts that look like this (the following data is for 2017 plans): The average deductible across the available plans is $245.66 and the highest is $500; the average out-of-pocket maximum is $660.94 and the highest is $854. (Out-of-pocket maximums do not include premiums. They limit how much financial exposure enrollees have in terms of cost-sharing, after premiums.)

So while state officials claim that the cost-sharing would be "roughly equivalent," the out-of-pocket maximum for these exchange plans offer less protection for many beneficiaries than Medicaid does. For example, consider an individual who makes $12,500 a year: If she was being charged premiums at 2 percent of her income, the most that she could be charged in cost-sharing on a monthly basis is $35. Over the course of the year, that would work out to $360. If that same individual was on the exchange, the available plans average $660.94 as an out-of-pocket maximum (the lowest available on any plan is $425) — and that's only over the course of the year, with no protections for monthly/quarterly charges.

People who shift to plans offered by their employer will often have to pay a lot more in both premiums and cost-sharing.

So far we've discussed people moving to the exchange. But not everyone will be eligible to get subsidized coverage on the exchange. Some of the people in this group currently have health insurance offered to them by their employer. If that insurance meets two tests — it's considered "affordable" by the law and meets a "minimum value" standard in terms of coverage — then they are not allowed to get the premium credits and cost-sharing reductions that would make coverage on the exchange affordable for them.

The problem is that many of the plans that employers offer will not actually be affordable for this working-poor population. For a plan to be deemed affordable, premiums cannot exceed 9.69 percent of household income. That means that a plan could have premiums nearly five times what someone was paying under the 2-percent max allowable under Arkansas Works (and even more than that compared to the flat $13 premiums that the program is imposing this year). Under the Medicaid rules in the Arkansas Works waiver, the most that an individual right at the poverty line could be charged is $20; the most that a single mother of three could be charged is $40. But if those same beneficiaries got insurance through a plan at work, they could face employee-contribution premiums of up to $95 or $195, respectively, and would then not be allowed to shop on the exchange. They would have to find a way to pay those premiums or go without health insurance.

In addition to dramatically higher premiums, people left with no choice but to enroll in work-based plans would face dramatically higher cost-sharing as well. For a plan to meet the "minimum value" test, it only has to cover 60 percent of average expected costs, as opposed to 94 percent. That could mean $5,000 deductibles or $7,000 out-of-pocket maximums, crushing expenses for this population of working poor Arkansans. The Arkansas Works plans (and, with slightly less protection, the exchange plans) are designed to keep expenses reasonable for this population; many of the employer-sponsored plans that the governor wants to shift people to are simply recipes for bills that this group can't possibly afford to pay, leaving hospitals and others to pick up the uncompensated care tab.

Of course, the actual employee costs associated with employer-sponsored plans would vary widely from employer to employer, but in many cases, the premiums and cost-sharing will simply be too high for the people that the governor is kicking off Medicaid to afford. But there won't be other options: Employees offered these plans won't be eligible for subsidies on the exchange either. They'll have no choice but to go without health insurance, or try to scrape by paying more than they can afford for insurance that doesn't give them sufficient coverage. Ironically, given Hutchinson's stated objectives of encouraging work and employer-sponsored insurance, this situation means that the people who are punished the most by the governor's proposed changes are those who have jobs that offer health insurance.

Employer-sponsored insurance is not a magic wand in terms of coverage for this income level. Under the governor's plan, the state will return to the situation it was in before expanding Medicaid, when many of the working poor simply couldn't afford health insurance.

Many people will fall through the cracks and go without coverage.

All of the above assumes that the people who lose coverage successfully navigate the system and find their way to coverage alternatives. If you hear the governor talk about moving this population from Medicaid to the exchange, you might think it's as easy as pushing a button or flipping a switch. Unfortunately, it's not that simple. This transition will involve more than 60,000 people receiving the news that their coverage has been cancelled and having to sign up for a private plan. That's a transition that demands excellent communication and a massive outreach effort (and ideally education about how to navigate the remaining options). In the past, the Hutchinson administration has shown disinterest or incompetence when it comes to communication and outreach for this population. For example, vital information about Medicaid eligibility renewals was announced in 2015 by inscrutable letters, many of which were sent to incorrect addresses.

One common theme I've heard from beneficiaries in the years that I've been covering the private option is confusion — about enrollment, about renewal, about what plan they have, and so on. This transition is almost certain to produce additional confusion. People will inevitably get lost in the shuffle and end up with gaps in coverage. In similar transitions in other states, even with significant outreach efforts, that's exactly what happened. Attrition is inevitable, both because some people will no longer be able to afford the cost of insurance, but also because some people will fall through the cracks. The most likely end result is that the uninsured rate will increase.

Without outreach, those who do sign up may end up with worse coverage.

Signing up for health insurance on the exchange can also be a confusing process. That's especially true for this population, who may not have any experience purchasing private insurance and who have very particular options in terms of cost-sharing that can be tricky to navigate.

Here's the biggest problem they may face: It's only possible to get the cost-sharing reductions if they sign up for a Silver plan. But they can use their premium credit on any plan, including Bronze plans, which don't offer as much coverage. Applying those subsidies might make the Bronze plans have very low premiums, or even no premiums at all. But without cost-sharing reductions, the deductible might be $6,000, the out-of-pocket max might be $7,000. If you're not familiar with how deductibles and cost-sharing works, you might pick a Bronze plan with a slightly lower subsidized premium than the Silver plan, but end up with coverage too skimpy to offer real protection for someone at this income level. This is where a real commitment to outreach would be vital.

To continue coverage, the governor's plan depends on the continuation of Obamacare.

He would never put it this way, but Hutchinson's entire approach to this population presupposes that the Affordable Care Act stays in place. He wants to move a subset of people off of the Medicaid expansion (itself funded by Obamacare) and onto the subsidized exchanges funded by Obamacare. So it might be relevant to note that the White House and Republicans in Congress are currently trying to pass a repeal-and-replace plan that would disrupt and dismantle that very same exchange in ways that threaten affordable coverage for consumers who are poorer or sicker. The governor's plan throws people overboard and offers the exchange as a life raft, but TrumpCare would poke holes in that life raft and leave people to sink.

State savings come with a human cost.

The state pays for 5 percent of the costs of covering people on the Medicaid expansion this year, which eventually jumps up to 10 percent in 2020 and beyond (the feds pick up the rest of the tab). If Hutchinson kicks 60,000 people off of the Medicaid expansion, it may save money for the state budget, but it will increase the number of uninsured Arkansans, increase uncompensated care costs and transfer the financial burden onto the state's working poor.

"Our greatest concern is that tens of thousands of Arkansans will become uninsured because they are no longer eligible for Arkansas Works, unable to afford other coverage, or simply fall through the cracks because of the constant policy changes," Marquita Little, of Arkansas Advocates for Children and Families, said. "We are not making our health care system better by increasing the number of uninsured people, driving up premiums, and adding to uncompensated care for providers."

This reporting is courtesy of the Arkansas Nonprofit News Network, an independent, nonpartisan news project dedicated to producing journalism that matters to Arkansans.